en

en

da

da

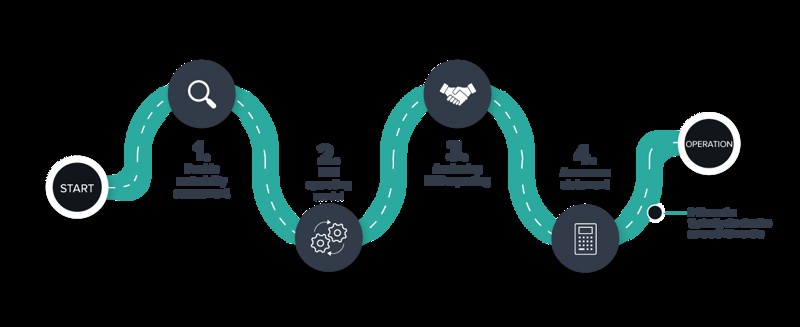

Your ESG roadmap from startup to annual report

In your role as a CFO or financial leader, you must manage the new requirements for sustainability reporting and achieve CSRD compliance. You might be wondering how best to start the process and which areas require extra focus to ensure effective implementation. Whether you need to build ESG reporting from scratch or upgrade an existing reporting process, help is available.

In this article, you can read our insights from our own practical experience structuring the task – for the road to achieving CSRD compliance is surprisingly uniform. With the right approach and an aligned level of ambition, you can streamline the process and save valuable working hours.

ESG-roadmap

1. Create insight and focus with the materiality assessment

As the CSRD provisions have taken shape, the concept of double materiality assessment (DMA) has never been more relevant.

It is no longer about navigating through long lists of mandatory KPIs; rather, focus has shifted to a more targeted and sharp approach with your DMA.

DMA is the first step towards CSRD compliance and is crucial for defining a relevant scope establishing the material aspects significant to your organisation and your stakeholders. Additionally, the DMA enables a strategic prioritisation of your activities and resources on the ESG areas where your company has a significant impact, risk, or opportunity.

Therefore, you can begin the CSRD process with a thorough and well-structured DMA, as it lays the foundation for all subsequent phases and also needs to be audited – both in terms of results and process. We recommend continuously aligning with your auditor to ensure that you don’t build a new reporting engine based on an incorrect reporting basis.

2. The ESG operating model helps you integrate your ESG reporting

With a clearly defined scope from your double materiality assessment, it is time for the next phase.

This is where the ESG operating model which should be able to support your company's specific reporting requirements enters the picture. Some of the key elements to establish in the operating model include internal organisation, resources, annual cycle, and – last but not least – the preparation of an ESG accounting manual.

The ESG accounting manual, which is also an invaluable tool in your collaboration with the auditor, should include details about your ESG KPIs, such as accounting practices, process descriptions, estimation principles, controlling steps, and the distribution of roles and responsibilities, if relevant.

To ensure that your reporting is both accurate, consistent, and precise, we recommend implementing processes and systems across the organisation and including regular controls that guarantee standardised data quality assurance.

By having clear roles and responsibilities, you also ensure that each link in the reporting chain contributes effectively to the ESG reporting and does not overlap more than necessary with, for example, the annual report.

Therefore, we also recommend that the coordinating task and the final responsibility lie within Finance, though many other parts of the ESG reporting are distributed throughout the organisation.

3. ESG reporting must be anchored across the board

Once you have created your ESG operating model, it is crucial to anchor it in your daily operations and decision-making processes.

By integrating ESG in both internal and external reporting, you get the opportunity to transform data into action and ensure that sustainability parameters become a natural part of your business case models.

With data insights, you can now set clear objectives, launch new initiatives, and establish a follow-up process to monitor your progress.

This approach creates a strong link between strategy and operational execution with continuous support and training, which is the foundation for successful implementation of ESG reporting.

4. Auditor's review

Navigating the auditor's requirements for CSRD compliance may seem like a major task. However, it is important to remember that this involves a statement with limited assurance, which is more similar to a review than a full audit.

The auditor must declare that, in performing the assurance engagement, they have not noticed any issues that would lead them to conclude that the sustainability reporting does not, in all material respects, comply with Section 99a of the Danish Financial Statements Act, including the ESRS and EU Taxonomy. And that the reporting has been prepared in accordance with the described process for identifying the relevant information (the DMA).

However, it should be emphasised that in the first year, there will be more extensive work regarding samples, as the auditor does not have previously audited data, accounting practices, internal processes etc., and there is no previous audit to "lean on."

Start with small and well-considered steps

As you can probably sense, the list of tasks is long in the transition towards CSRD-compliant reporting.

Therefore, we recommend keeping the reporting scope at a practical and reasonable level initially.

This means that you need to maintain a sharp focus throughout the DMA process and turn your attention to the most significant aspects.

By prioritising and having the key elements in place first, you can always expand your reporting with additional 'nice-to-have' KPIs and become more ambitious over time.

Once your reporting engine has been established, calibrated, and tested, and once the rest of the organisation is prepared for ESG reporting, everything becomes easier to approach.

Achieving CSRD compliance is a comprehensive task, so make sure to maintain a pragmatic perspective and ensure a reasonable approach to CSRD reporting in your company – even that is ambitious.

Do you need help achieving CSRD compliance?

Feel free to contact us for a non-binding dialogue on how we can assist you with your ESG reporting – including implementation of an ESG roadmap from start-up to assurance statement.